Understanding Insurance Claims for Water Damage in Castle Rock, Colorado and Nearby Areas

Water damage can happen unexpectedly due to burst pipes, appliance leaks, heavy storms, or plumbing failures. When such incidents occur, homeowners often rely on their insurance policies to help cover repair and restoration costs. However, understanding how insurance claims work for water damage is important to ensure a smooth process. Knowing what steps to take and what coverage typically includes can help property owners handle claims more efficiently.

What types of water damage are usually covered by homeowners insurance?

Most homeowners insurance policies cover sudden and accidental water damage. This may include issues such as burst pipes, plumbing leaks, or water damage caused by malfunctioning appliances. Coverage generally applies when the event is unexpected and not due to neglect. Reviewing the details of your policy helps clarify what types of incidents are included.

Why is it important to report water damage quickly to your insurer?

Reporting water damage as soon as possible helps start the claims process quickly. Insurance providers often require prompt notification to evaluate the damage properly. Early reporting also helps prevent further damage to the property. Acting quickly ensures that documentation and inspection can be completed in time.

How should homeowners document water damage before filing a claim?

Proper documentation is essential for a successful insurance claim. Homeowners should take clear photos and videos of affected areas and damaged items. Keeping records of repair estimates and restoration services also helps support the claim. Detailed documentation provides evidence for the insurance company during the evaluation process.

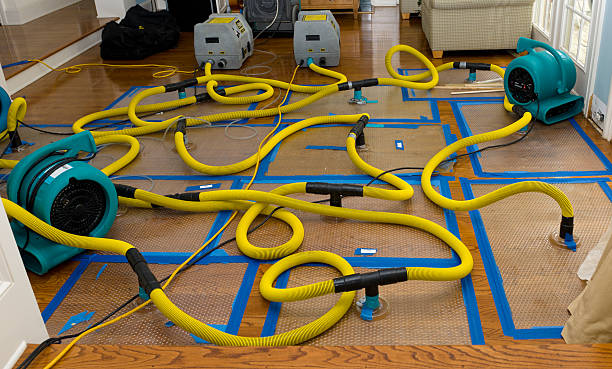

What role does a professional water restoration company play in the claim process?

Professional restoration companies often assist homeowners by assessing the extent of the damage. They may provide written reports, cost estimates, and documentation required by insurance providers. Their expertise helps identify hidden moisture and structural damage. This information can strengthen the insurance claim.

How does the insurance adjuster evaluate water damage claims?

After a claim is filed, an insurance adjuster typically visits the property to inspect the damage. The adjuster reviews documentation, examines affected areas, and estimates repair costs. Their evaluation helps determine the amount of coverage available. Accurate inspection ensures fair claim processing.

Why might some water damage claims be denied?

Claims may be denied if the damage resulted from lack of maintenance or gradual leaks that were ignored over time. Many policies also exclude damage caused by flooding unless separate flood insurance is purchased. Understanding policy limitations helps avoid misunderstandings during the claim process.

How can homeowners reduce additional damage while waiting for claim approval?

Homeowners should take reasonable steps to prevent further damage after a water incident. This may include turning off the water supply, removing standing water, or covering damaged areas temporarily. Insurance companies often expect homeowners to protect their property from worsening conditions. These actions can support the claim.

What expenses may be covered by water damage insurance claims?

Depending on the policy, insurance may cover structural repairs, damaged flooring, drywall replacement, and restoration services. In some cases, temporary living expenses may also be covered if the home becomes uninhabitable. The exact coverage varies by policy. Reviewing the policy details helps clarify what is included.

Why is understanding your policy deductible important?

The deductible is the amount the homeowner must pay before insurance coverage begins. Knowing this amount helps determine how much financial responsibility the homeowner has during repairs. Higher deductibles may reduce insurance premiums but increase out-of-pocket costs during a claim. Understanding this detail helps with financial planning.

How can homeowners prepare for future water damage claims?

Regular plumbing inspections, proper maintenance, and installing water leak detection systems can reduce risks. Keeping updated records of home repairs and insurance documents also helps during future claims. Being prepared allows homeowners to respond quickly if water damage occurs again.

Final Thought

Understanding how insurance claims work for water damage can make the recovery process less stressful for homeowners. Proper documentation, quick reporting, and professional restoration services all play important roles in successful claims. Reviewing insurance policies carefully helps homeowners know what coverage they have and what limitations may apply. With the right preparation and knowledge, property owners can handle water damage claims more confidently.

Does homeowners insurance cover flooding from heavy rain?

Standard homeowners insurance usually does not cover flooding from natural disasters, but separate flood insurance policies may provide coverage.

How long does the water damage insurance claim process take?

The timeline varies depending on the extent of damage and documentation, but many claims are processed within several weeks.

Can I start repairs before the insurance adjuster visits?

Emergency steps to prevent further damage are usually allowed, but major repairs should wait until the adjuster completes the inspection.

Do restoration companies work directly with insurance providers?

Many restoration companies help homeowners by providing documentation and communicating with insurance providers during the claim process.

What should I do immediately after discovering water damage?

Turn off the water source if possible, document the damage, and contact your insurance provider to start the claims process.

- Here's some stuff

- Here's some stuff